The Middle East and Russia will be among the last suppliers of hydrocarbons

Amid increasing electrification, the energy dependence of OECD countries and China on their major hydrocarbon suppliers, the Middle East and Russia, could increase. Indeed, even in "Net Zero" scenarios, the world will continue to consume fossil fuels. While this consumption will drop drastically compared to today, oil and natural gas production will be concentrated in a smaller number of countries.

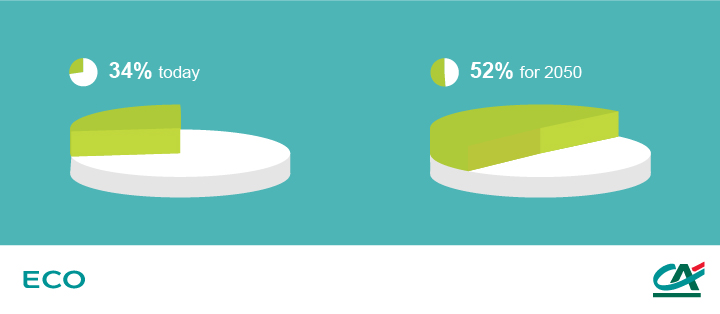

OPEC'S SHARE OF WORLD OIL PRODUCTION

Indeed, countries with high production costs will no longer be able to maintain themselves in the face of falling demand. Also, on the basis of their production costs and their volumes of proven oil and natural gas reserves, the Middle East and Russia will likely be among the last suppliers of hydrocarbons. The International Energy Agency (IEA), in its "Net Zero" scenario published last June, forecasts an increase in exposure to OPEC. The cartel’s production is expected to stand at 52% of world oil consumption in 2050, compared to 34% today.

South America, Africa, Australia and Asia to benefit from growing demand for non-ferrous metals

The development of fossil fuels has focused on steel. In fact, oil pipelines, gas pipelines, piping and equipment for treatment facilities, offshore platforms, tankers and even cars are essentially made of steel. While steel will always remain important to the economy, decarbonisation will lead to increased demand for many non-ferrous metals such as cobalt, copper, lithium, rare earth elements and even aluminium.

Electrification, a pillar of decarbonisation, will require the construction of numerous wind farms and power lines. The various "Net Zero" scenarios are based in particular on significant development of offshore wind power, which consumes a high volume of rare earth elements to produce permanent magnets, a technology currently favoured by wind turbine manufacturers for offshore applications. The thousands of km of electric cables to be installed will be made of copper or aluminium. The batteries that are essential for powering mobility and storing electrical energy will contain lithium, cobalt, nickel and aluminium. To make them more lightweight, thus increasing their range, electric cars will incorporate more aluminium than their predecessors, internal-combustion cars.

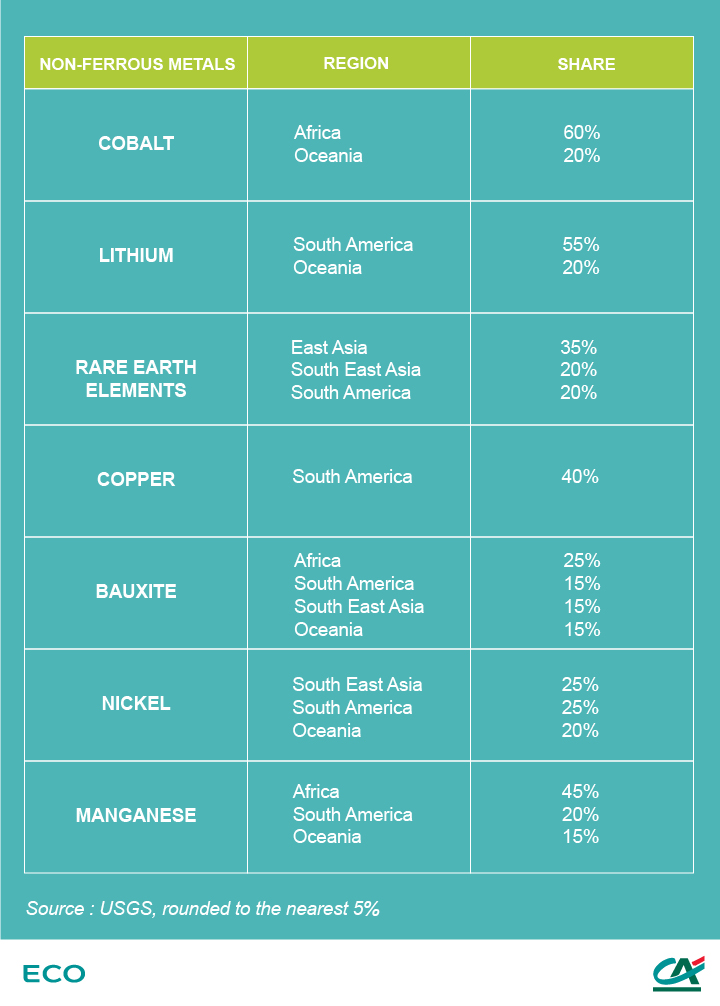

LARGE AREAS OF NON-FERROUS METAL RESERVES

By analysing the distribution of non-ferrous metal reserves that will be used in decarbonisation, we see how prominent South America, Africa, Australia and Asia will be on the international geopolitical scene. Unfortunately, Europe will not be a major player in the supply of non-ferrous metals and will have to rely mainly on foreign supply.

Geopolitics specific to the energy transition will overlap with the geopolitics of oil and natural gas

Even though decarbonisation will generally reduce dependence on foreign energy, the geopolitics of energy will continue to influence international relations.

On the one hand, the majority of countries will remain dependent on the major suppliers of fossil fuels, the Middle East and Russia. As long as the armies, and therefore national security, depend on oil, it is very likely that oil will remain a strategic primary energy. Perhaps only the United States, with its untapped reserves of natural gas and bedrock oil, will be able to rely less on the Middle East for its oil and natural gas supply.

The geopolitics specific to the energy transition will overlap with the geopolitics of oil and natural gas, which should persist. These new geopolitics will share certain leading players (Middle East, Russia) with the geopolitics of oil and gas.

See also "Global economy – One Belt, One Road, new paths?" published by the Economic Research team, for a more detailed look at the current situation and outlook.

Winners and losers

Brazil, now a major oil producer, is expected to remain a key player in the energy supply chain thanks to its biomass, rare earth element resources, manganese, nickel and aluminium bauxite. This is also the case for Australia, which holds large reserves of most of the non-ferrous metals needed to electrify economies. Norway, a major supplier of oil and natural gas to Europe, is also expected to remain a key player in European energy policy, thanks to its wind and water resources.

And new countries are expected to appear on this new energy scene. This includes some African countries, such as the Democratic Republic of Congo, Guinea, and Zambia. In South America, Chile will undoubtedly be a new promised land for energy. In addition to exceptional sunshine in certain regions, Chile also has the largest reserves of copper and lithium. Cuba, with the third largest reserve of cobalt, may spark new interest from the United States. In North Africa, while oil and natural gas reserves were mainly concentrated in Algeria and Libya, Morocco and Tunisia could become energy suppliers to Europe.

Other countries could fall out of geopolitical view. Nigeria and Angola, major producers of oil and natural gas in West and Central Africa, could fall victim to decarbonisation. Given that they produce hydrocarbons that are more expensive than those in the Middle East, have low non-ferrous metal reserves, and are subject to low winds and average sunshine, these two countries are likely to find themselves downgraded.

What about Europe? Its future depends on its expertise in decarbonisation technology

Europe will enjoy an improvement in its energy autonomy, largely due to offshore wind power for northern Europe and solar power for southern Europe. However, it will remain dependent on renewable primary energy resources and non-ferrous metals from abroad. For Europe, then, decarbonisation will certainly not equal energy independence. Therefore, technological expertise is a key issue. For the European ‘concert of nations’, it is a question of staying one step ahead in a rapidly changing world.