Concentrated fossil fuel reserves make consumer countries vulnerable

Fossil fuels have played a key role in the economics and development of the consumer society. Of these, oil is used not only in the production of the fuels that make almost all our travel possible, but some of its by-products form the basis of the plastics found in many consumer goods. Global economic growth over the past twenty years has been accompanied by a sharp increase in demand for oil: between 2000 and 2019, it increased by 20%, with almost half of the increase coming from growing Chinese demand.

However, reserves of oil, natural gas and coal are poorly distributed geographically. This means a large number of consumer countries become very highly dependent on, and vulnerable to, a small number of producer countries. This is perfectly illustrated by the oil shocks of 1973 and 1979, which put an end to the economic growth of the post-war period. Therefore, fossil fuels are a leading economic and geopolitical weapon. Indeed, the geopolitical role that oil played during the 20th century has a long history.

Decarbonisation will not mark the end of energy geopolitics

The phase-out of fossil fuels, which is part and parcel of decarbonising the economy, is, logically, seen as a means for fossil fuel consumer countries to become more energy-independent. Decarbonisation would also put an end to oil revenue’s negative economic and societal effects on the producer countries. However, there is no guarantee that decarbonisation will spell the end of energy geopolitics.

As all countries are more or less sunny and windy, each country will be able to produce some of the energy its economy needs to function. No country should remain 100% dependent on energy imports for its primary energy supply, as is the case today. However, while all countries should be moving toward energy independence, decarbonisation cannot provide it for all. As with fossil fuels, large renewable energy resources are not evenly distributed.

Russia, the Middle East, North Africa, and Australia boast abundant renewable energy resources

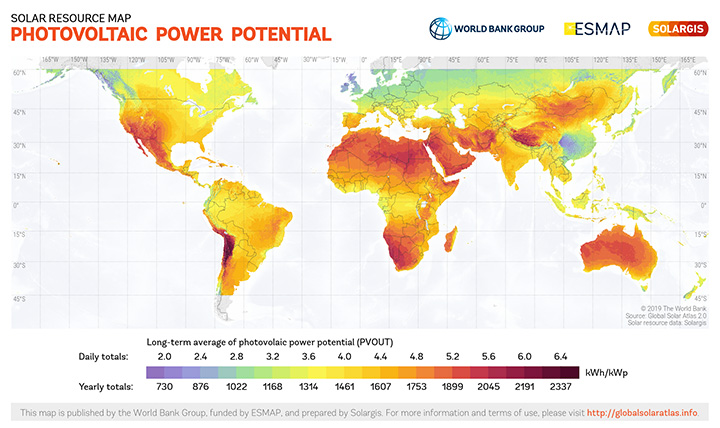

SOLAR POTENTIAL

Source : Global Solar Atlas (1)

WIND POTENTIAL

Source : Global Wind Atlas (2)

The regions located between the ±15° parallels have relatively little wind, and weak solar potential. Conversely, countries located in subtropical regions enjoy ample sunshine and, near the coasts, favourable wind patterns. Countries located at higher latitudes may also have good wind conditions near the coast, but less sunshine.

The solar and wind energy production potential for a country also depends on its land mass. Thus, Russia has a large reservoir of land and solar wind energy thanks to its gigantic surface area. The Middle East, North Africa and Australia, all major fossil fuel exporters, also have significant renewable energy resources – especially solar.

Europe, the United States, Japan, South Korea and China will remain energy-dependent

Despite their solar, wind or biomass resources, Europe, the United States, Japan, South Korea and China may well be unable to achieve total energy independence, given that they have so many high-consumption sectors such as transport and residential heating. Therefore, these countries should continue to import some of the energy they consume.

However, with the exception of biomass, renewable energy cannot be transported in its primary forms (irradiation, winds). It will have to be transformed into electrons or another energy carrier such as hydrogen to be transported from one country to another. Certainly, major power lines could be run from North Africa or even Russia to supply Europe. Over greater distances, the use of hydrogen and its derivatives is currently being considered in all low-carbon scenarios.

Freshwater resources are often insufficient for hydrogen-producing countries to export to energy-consuming countries

In the more distant future, to produce hydrogen by electrolysis or perhaps by photocatalysis (3), water will be needed. As such, the strategic value of water is likely to increase in the coming decades. To become a hydrogen exporter, a country will need not only strong renewable energy potential, but also access to large water reserves.

The distribution of water resources is unbalanced. The Middle East, North Africa, Australia, and Chile have strong solar and wind potential. Unfortunately, access to fresh water is difficult there. These regions are particularly arid and must also cope with growing fresh water needs for their people, agriculture and industries.

Access to the sea is an asset for some countries

Australia, North Africa and Chile could become more arid if global warming exceeds 2°C. However, with their coastal access to seawater, these countries should be able to produce the water they need to produce hydrogen, at the cost of lower energy efficiency and increased production costs. Therefore, the Middle East, North Africa, Australia and Chile should be well-positioned to create renewable energy export infrastructures. Recent announcements of hydrogen mega-projects seem to confirm manufacturer and investor preference for these regions.

(1) Map obtained from the Global Solar Atlas 2.0, a free, web-based application developed and operated by the Solargis s.r.o. on behalf of the World Bank Group, utilizing Solargis data, with funds provided by the Energy Sector Management Assistance Program (ESMAP). For additional information: https://globalsoalratlas.info

(2) Map obtained from the Global Wind Atlas 3.0, a free, web-based application developed, owned and operated by the Technical University of Denmark (DTU). The Global Wind Atlas 3.0 is released in partnership with the World Bank Group, utilizing data provided by Vortex, using funding provided by the Energy Sector Management Assistance Program (ESMAP). For additional information: https://globalwindatlas.info

(3) Using photocatalysis to break down water into its hydrogen (H2) and oxygen (O2) molecules means using photons energetic enough to crack water molecules (H2O).